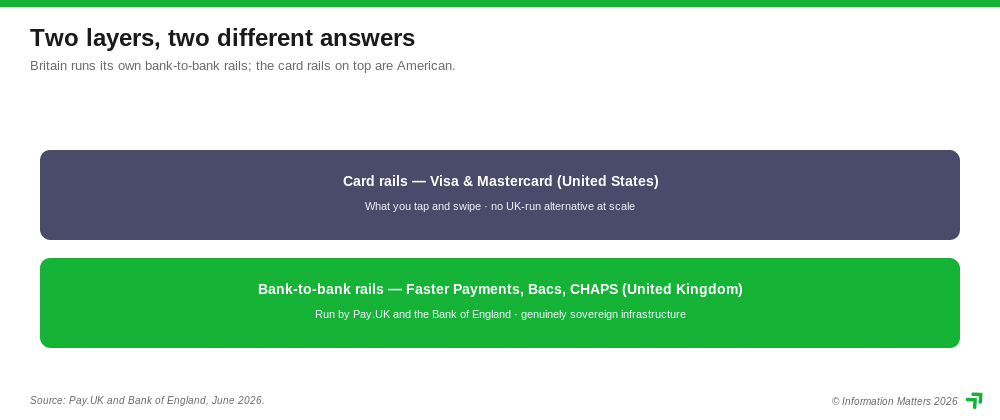

The rails are British. The cards are not.

Every time money moves in Britain, it travels on one of two kinds of track. The bank-to-bank rails — Faster Payments, Bacs, CHAPS — are genuinely home-grown, run by a UK not-for-profit and the Bank of England. The card schemes almost everyone actually taps and swipes — Visa and Mastercard — are American, and no UK merchant can route around them. We looked at the networks that move the money to ask which layer Britain really controls, and which it only rents.

Most sovereignty questions in this series end the same way: the software is foreign, the data sits abroad, the escape routes are thin. Payments are the exception that proves how rare genuine sovereign infrastructure is. Here, for once, Britain owns the road — the wholesale and retail bank-to-bank rails are run domestically, under public or industry governance. But the layer the public sees and uses every day, the card network, is a near-total American duopoly. The contrast inside one category is the whole story.

The layer Britain actually runs

Start with the good news, because there is some. The systems that clear and settle sterling between banks are run from Britain, by British bodies.

Pay.UK — a company limited by guarantee (a not-for-profit structure), the recognised operator of the country’s interbank retail payment systems — runs Bacs (Direct Debit and Bacs Direct Credit, the rails behind salaries, pensions and most household bills), the Faster Payment System (the instant transfers behind your banking app), the Image Clearing System (digital cheque processing) and the Current Account Switch Service. By its own account it enables billions of pounds of payments, safely and securely, every single day, and it is supervised by the Bank of England’s Financial Market Infrastructure Directorate and regulated by the Payment Systems Regulator. This is national infrastructure, governed in the national interest.

Above it sits CHAPS, the sterling same-day system for high-value and time-critical payments — the rail your solicitor uses to complete a house purchase. CHAPS is operated directly by the Bank of England, which took over responsibility in November 2017, and settles in the Bank’s own real-time gross settlement (RTGS) system. You cannot get more sovereign than a payment rail run by the central bank.

So far, so British. Then comes the catch.

The American company inside the British rails

The rails are British-governed. The technology that actually runs two of them is not. The platforms that power Bacs and the Faster Payment System are built and operated by Vocalink — and Vocalink, in its own words, is “a Mastercard company.” Mastercard acquired it in 2016 (completing 2017). So while Pay.UK sets the rules and owns the schemes, the day-to-day processing engine behind Britain’s instant payments and Direct Debits is operated by a subsidiary of a New-York-listed American corporation.

This is the sharp edge of the sovereignty question. Governance can be British while the operating technology answers to a US parent — and a US parent is, in principle, reachable by US legal process such as the CLOUD Act (the law that lets American authorities compel US companies to hand over data they control, wherever it is held). The rail is ours; the company keeping it running is not. It is the single most important nuance in the whole category.

The duopoly you cannot route around

Now the part everyone touches. When a card is tapped, swiped or entered online in Britain, the transaction almost always rides Visa (Visa Inc., listed in New York as NYSE: V) or Mastercard (Mastercard Incorporated, NYSE: MA). Both are American public companies. Between them they carry the overwhelming majority of UK card payments, and there is no domestic card scheme of comparable scale to switch to. A British merchant who wants to accept cards has, in practice, no UK-run alternative network. This is the most concentrated foreign dependency in the entire payments stack — and the least escapable.

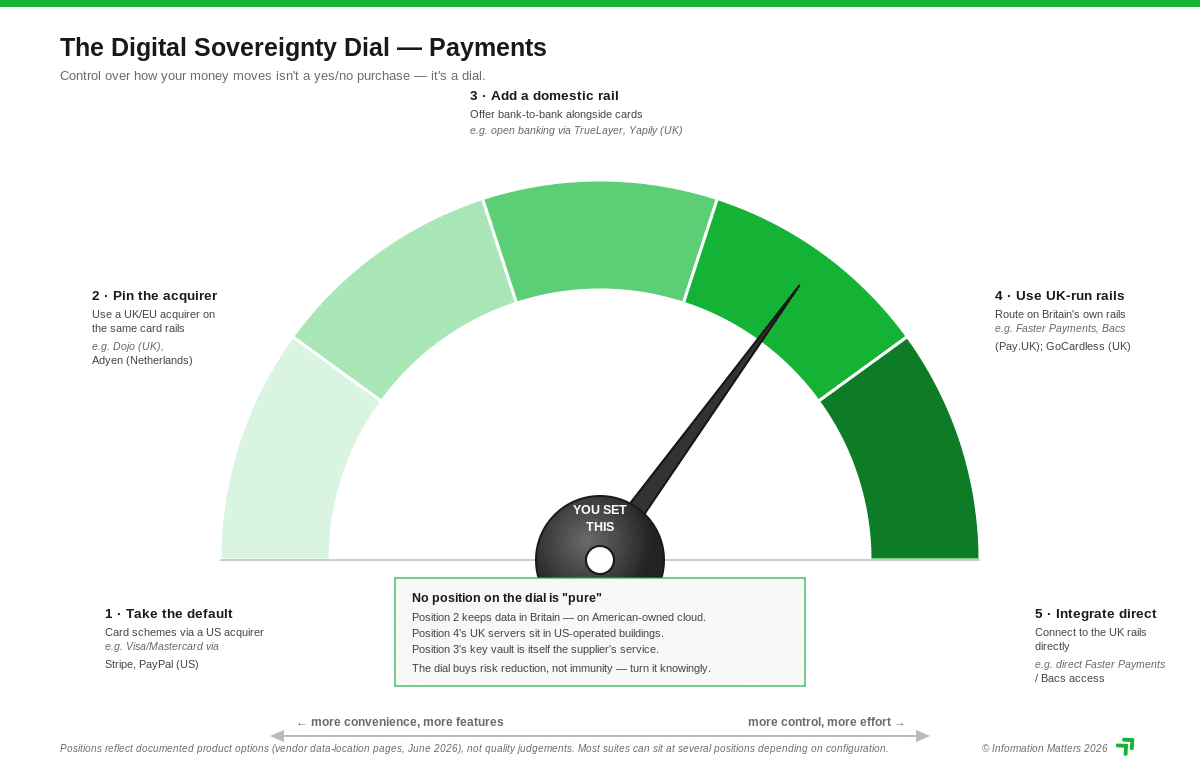

The one genuine alternative path: open banking

There is one route that bypasses the card schemes entirely: open banking — paying straight from your bank account to the merchant’s, over the UK’s own Faster Payments rail, with no card network in the middle. (The technical term is a payment initiation service provider, or PISP — software that, with your permission, instructs your bank to make a payment.)

And here the ownership news is encouraging. The leading UK open-banking providers are UK-controlled. TrueLayer (TrueLayer Group Holdings Limited, London) records no single controlling person at Companies House — venture-backed with no dominant owner. Yapily (Yapily Ltd, London) records a single active person with significant control — its UK-resident founder. Moneyhub (Moneyhub Holdings Ltd, Bristol) likewise records no single registrable controller. These are British companies, routing British payments over British rails.

The caveat: this layer is not uniformly home-grown. Plaid is American. Tink, a prominent account-to-account and data provider, is owned by Visa — the card duopoly buying into the very rail meant to bypass it. So even the alternative path has American ownership threaded through it.

The acquirers sit on top — and they are mostly foreign

Between the merchant and the schemes sits the acquirer or processor — the company that actually takes the card payment and moves the money. This layer is crowded and largely foreign-owned. Stripe (US), Adyen (Netherlands, listed in Amsterdam), Worldpay (now under US-listed Global Payments Inc.), Block/Square (US), PayPal (US) and SumUp (Luxembourg) dominate. The genuinely UK-controlled options are fewer: Dojo trades through a London company (Paymentsense Limited) but sits under a Jersey holding structure (Typhoon Topco); Teya is UK-registered (founder-private); GoCardless (GoCardless Holdings (UK) Limited) records no single registrable controller at Companies House — though an acquisition by the Dutch payments group Mollie has been announced and is not yet reflected on the register, so this is one to watch. The familiar British high-street card terminal is, more often than not, processed by a company headquartered abroad.

At a glance

| Network / Provider | Controlled from | UK-run? | What it does | Notes |

|---|---|---|---|---|

| Faster Payment System (Pay.UK) [1] | UK | Yes — Pay.UK | Instant bank-to-bank transfers | Scheme UK-run; platform operated by Vocalink, a Mastercard company |

| Bacs (Pay.UK) [1] | UK | Yes — Pay.UK | Direct Debit & Direct Credit (salaries, bills) | Same: UK scheme, Vocalink (Mastercard) platform |

| Image Clearing System (Pay.UK) [1] | UK | Yes — Pay.UK | Digital cheque clearing | UK-run |

| CHAPS [2] | UK | Yes — Bank of England | High-value same-day sterling settlement | Run by the central bank; settles in RTGS |

| Vocalink [3] | USA (Mastercard) | Operates UK rails | Builds/runs Bacs & FPS platforms | “A Mastercard company”; Mastercard Inc. NYSE: MA |

| Visa [4] | USA (listed) | No | Card payment network (VisaNet) | NYSE: V; no UK-run alternative at scale |

| Mastercard [5] | USA (listed) | No | Card payment network | NYSE: MA; no UK-run alternative at scale |

| TrueLayer [6] | UK | Yes | Open banking — pay direct from bank account | No single registrable controller (VC-backed) |

| Yapily [7] | UK | Yes | Open banking payments & data | UK founder-controlled |

| Moneyhub [8] | UK | Yes | Open finance data & payment initiation | No single registrable controller (VC-backed) |

| GoCardless [9] | UK | Yes | Bank-to-bank payments (Direct Debit, open banking) | UK VC-backed; no single registrable controller. Mollie (NL) acquisition announced, not yet on the register — watch |

| Plaid [10] | USA | No | Bank-account connectivity & data | US-controlled |

| Tink [11] | Sweden (Tink AB) — US-owned | No | Account-to-account payments & data | Wholly owned by Visa (since 2022) |

| Stripe [12] | USA | No | Acquiring & processing | Founder-private; no UK data region |

| Adyen [13] | Netherlands (listed) | No | Acquiring & processing | Euronext Amsterdam |

| Worldpay [14] | USA | No | Merchant acquiring & processing | Under Global Payments Inc. |

| Dojo [15] | UK operating co — Jersey topco | Partly | SME card acquiring & terminals | Paymentsense Ltd (London) under Typhoon Topco (Jersey) |

| SumUp [16] | Luxembourg | No | Card readers & acquiring | — |

| Teya [17] | UK | Yes | Card machines & acquiring | UK founder-private |

| PayPal [18] | USA (listed) | No | Online payments & card processing | NASDAQ: PYPL |

The escape routes are real — but only on one layer

The honest summary is layer-by-layer. On the bank-to-bank rails, Britain already has sovereign infrastructure: Pay.UK and the Bank of England run the schemes, and open banking lets a merchant accept payment straight over Faster Payments using a UK-controlled provider (TrueLayer, Yapily, Moneyhub, GoCardless). For payments that suit account-to-account — recurring bills, invoices, higher-value e-commerce — this is a genuine, home-grown alternative to the card networks, and it is the one place in this series where “buy British” is actually available at scale.

On the card schemes, there is no escape route at all. If you need to accept cards — and almost every consumer-facing business does — you are on Visa or Mastercard, and you are American-dependent by default. The most you can do is reduce how much of your volume rides the cards by steering suitable payments to open banking.

And one dependency hides inside the good news: even the British rails run on Vocalink, a Mastercard subsidiary. Sovereignty of governance is not the same as sovereignty of operation.

What buyers should take from this

The dial applies, but it works differently here because the layers diverge so sharply. A UK business choosing how to take money should ask: what share of our payments truly needs a card, and what share could ride open banking over Faster Payments instead? If we want a UK-controlled provider, is our open-banking or acquiring partner actually UK-owned (TrueLayer, Yapily, Moneyhub, GoCardless, Teya) rather than American with a British brand on the terminal? And do we understand that even the sovereign rails depend operationally on a Mastercard subsidiary?

For most businesses the realistic position is a blend: cards on Visa/Mastercard through an acquirer for the payments that need them, plus an open-banking path over the UK rails for the payments that don’t — chosen, where it matters, from a UK-controlled provider. That blend is the one place in this whole series where the sovereign option is not a compromise but a live, working alternative. The lesson the payments category adds is precise: Britain can and does run its own payment rails — but the cards on top of them, and the company inside them, are not ours.

Sources

All facts are taken from each operator’s or company’s own published pages and from UK company registers (Companies House) and the Bank of England, read directly during June 2026. One primary reference per entity.

- Pay.UK (Faster Payments, Bacs, Image Clearing System, Current Account Switch Service) — Pay.UK “Who we are”: https://www.wearepay.uk/who-we-are/

- CHAPS — Bank of England (operator since November 2017; RTGS settlement): https://www.bankofengland.co.uk/payment-and-settlement/chaps

- Vocalink (“a Mastercard company”; operates Bacs & Faster Payments platforms) — Vocalink “About us”: https://www.vocalink.com/about-us/

- Visa — Visa Inc., NYSE: V (US-listed corporation): https://investor.visa.com/

- Mastercard — Mastercard Incorporated, NYSE: MA (US-listed corporation): https://www.mastercard.com/news/about/

- TrueLayer — Companies House, TrueLayer Group Holdings Limited (12500702), persons with significant control (no registrable controller): https://find-and-update.company-information.service.gov.uk/company/12500702/persons-with-significant-control

- Yapily — Companies House, Yapily Ltd (10842280), persons with significant control (UK-resident founder PSC): https://find-and-update.company-information.service.gov.uk/company/10842280/persons-with-significant-control

- Moneyhub — Companies House, Moneyhub Holdings Ltd (11087893), persons with significant control (no registrable controller): https://find-and-update.company-information.service.gov.uk/company/11087893/persons-with-significant-control

- GoCardless — Companies House, GoCardless Holdings (UK) Ltd (15938440), persons with significant control (active statement: no registrable controller; Mollie acquisition announced, not yet on register): https://find-and-update.company-information.service.gov.uk/company/15938440/persons-with-significant-control

- Plaid — Plaid, Inc. (US company): https://plaid.com/

- Tink (wholly owned by Visa since 2022; Tink AB, Stockholm) — Tink “About us”: https://tink.com/about-us/

- Stripe — Stripe, Inc. (US, founder-private): https://stripe.com/

- Adyen — Adyen N.V., Euronext Amsterdam: https://www.adyen.com/investor-relations

- Worldpay (under Global Payments Inc.) — Global Payments: https://www.globalpayments.com/

- Dojo — Companies House, Paymentsense Limited (06730690), persons with significant control (Hurricane Bidco Limited; ultimate Jersey topco): https://find-and-update.company-information.service.gov.uk/company/06730690/persons-with-significant-control

- SumUp — SumUp (Luxembourg): https://www.sumup.com/

- Teya — Companies House, Teya (search): https://find-and-update.company-information.service.gov.uk/search?q=teya

- PayPal — PayPal Holdings, Inc., NASDAQ: PYPL: https://investor.pypl.com/

Research notes: all facts from operators’ and companies’ own published pages, the Bank of England, and Companies House, read directly during June 2026. Several open-banking and acquiring providers are venture-backed with no single registrable controller — recorded as “no single controller,” not as a named owner. Ownership and operating arrangements change; check current filings before relying on them. This article reflects the opinions of the Information Matters team — human and AI — and should not be considered statements of fact.

If you have any questions or comments about this article please email info@informationmatters.net