The transition from generative AI to agentic systems represents a fundamental shift in the enterprise technology stack—moving from models that summarize information to systems that autonomously execute multi-step workflows. As we move into 2026, the “agentic economy” is transitioning from speculative pilot projects to a structured, high-value market. This shift is characterized by a move toward reasoning, planning, and tool utilization, requiring a sophisticated architectural stack to manage the resulting complexity.

Agentic AI Market Research

The financial trajectory for this sector suggests a massive expansion, though the pace of adoption varies significantly by layer. International Data Corporation (IDC) provides a staggering look at the scale of this “digital workforce,” forecasting that the number of active AI agents globally will rise from roughly 28 million in 2025 to over 2.2 billion by 2030. While the raw number of agents is impressive, the work volume is even more notable; IDC expects the annual number of tasks executed by these systems to grow at a 524% CAGR, reaching 415 trillion by the end of the decade.

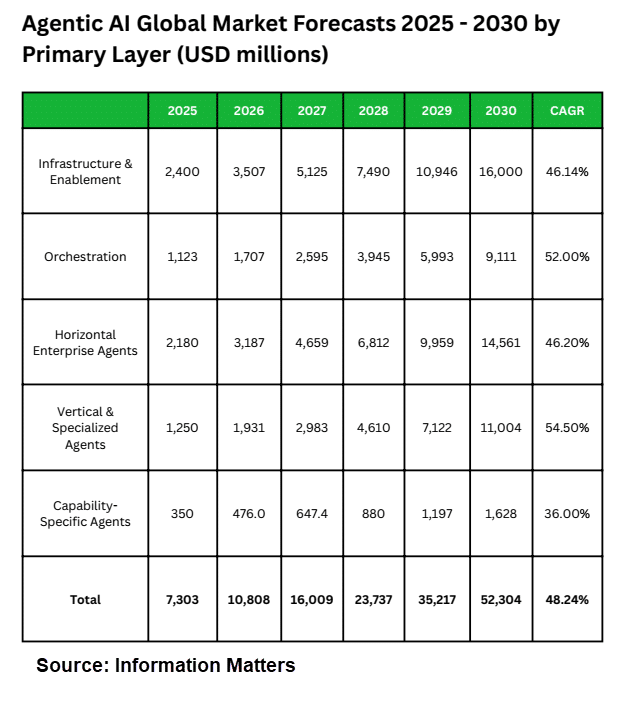

From a valuation perspective, Information Matters estimates the global market for agentic AI solutions at approximately $7.3 billion in 2025, with projections pushing toward $52.3 billion by 2030. Within this market, the orchestration layer—which manages how disparate agents communicate and maintain state—is expected to be the fastest-growing segment. This aligns with the hypothesis that the primary value is no longer just in “building” an agent, but in managing the collaborative friction between specialized autonomous teams. Boston Consulting Group (BCG) adds that 90% of CEOs expect to see measurable ROI from these investments as early as 2026, leading many to commit over 30% of their total AI budgets specifically to agentic capabilities.

Agentic AI Deployments

Real-world deployments are currently concentrated in sectors with high-volume, structured workflows. Capgemini research highlights that 82% of organizations plan to integrate AI agents within the next three years, with 10% already operating active workflows. These deployments are increasingly focused on “ready-to-deploy” models. Information Matters notes that nearly 64% of the current market is dominated by off-the-shelf agents, as enterprises seek to bypass the high costs and internal skills gaps associated with custom-built solutions.

In the retail sector, the impact is expected to be transformative. Bain & Company forecasts that by 2030, AI agents could mediate between 15% and 25% of all U.S. e-commerce sales. This represents a shift from “personalization”—where a human is shown tailored options—to “delegation,” where the agent autonomously researches, compares, and completes the purchase. McKinsey & Company describes this as the “agentic commerce” era, noting that for merchants, the priority is shifting toward making product data machine-readable. If a retailer’s inventory cannot be understood by an agent, it effectively becomes invisible to a significant portion of the future market.

The vendor landscape is evolving to support a “Build-Deploy-Run” lifecycle that is more complex than standard SaaS. BCG identifies a $200 billion net new demand for technology services specifically to support the integration of agents into legacy systems like ERP and CRM. This demand is driven by the need for specialized workflow engineering and “knowledge codification”—translating institutional human knowledge into structured data that an agent can act upon.

Major software vendors are already moving to capture this. Capgemini points to SAP as a primary example of a legacy provider aggressively embedding agentic development tools and specialized agents directly into its core ERP systems. This suggests that the next generation of enterprise software will not be a tool used by humans, but an environment inhabited and managed by agents. This trend reinforces the idea that the “orchestration” of these systems will become the dominant bottleneck for vendors, as they move from providing standalone “copilots” to managing complex agentic swarms.

As agents gain the autonomy to move money and access sensitive data, security and reliability have become the primary hurdles to adoption. Information Matters highlights a significant “trust gap”: while 38% of users trust agents for routine data analysis, that figure drops to just 20% for high-stakes interactions like financial transactions. This lack of trust is a major headwind for autonomous systems and underscores why the “Infrastructure & Enablement” layer—specifically for evaluation and observability—is seeing such high investment.

From a legal and risk management perspective, the complexity of multi-step autonomous workflows increases the potential for “agentic drift” or cascading errors. BCG notes that successful deployment requires robust “human-in-the-loop” (HITL) frameworks to manage risk. Furthermore, as McKinsey suggests, the legal implications of “agentic commerce” are still being defined. When an agent makes a purchase on behalf of a consumer, the traditional models of consumer protection and liability must be re-evaluated for a world where the “buyer” is not a human, but a piece of software acting on intent.

While the forecasts from IDC and Information Matters paint a picture of exponential growth, a measured “colleague-to-colleague” analysis suggests several points of friction. The leap from 44 billion tasks to 415 trillion assumes that the cost-per-task will drop significantly and that the energy and compute infrastructure can scale to meet this demand. There is a risk of “agentic boosterism”—the belief that agents will solve all productivity woes—while ignoring the reality that most corporate data is still too siloed and messy for an autonomous agent to navigate reliably.

The real winners in the next five years will not necessarily be the companies with the most agents, but those that master the orchestration layer and bridge the trust gap. As BCG and Capgemini data suggests, the move toward agentic AI is as much an organizational change as it is a technological one. Companies must move beyond the “chat” interface and focus on the deep integration, auditability, and process redesign required to let agents actually do the work.

Sources:

https://www.bain.com/insights/2030-forecast-how-agentic-ai-will-reshape-us-retail-snap-chart/

https://www.bcg.com/publications/2026/the-200-billion-dollar-ai-opportunity-in-tech-services

https://www.capgemini.com/insights/research-library/ai-agents/

https://www.bcg.com/capabilities/artificial-intelligence/ai-agents

https://my.idc.com/getdoc.jsp?containerId=prUS53765225